We Are Becoming the “New Poor.” What Can We Do About It?

We Are Becoming the “New Poor.” What Can We Do About It?

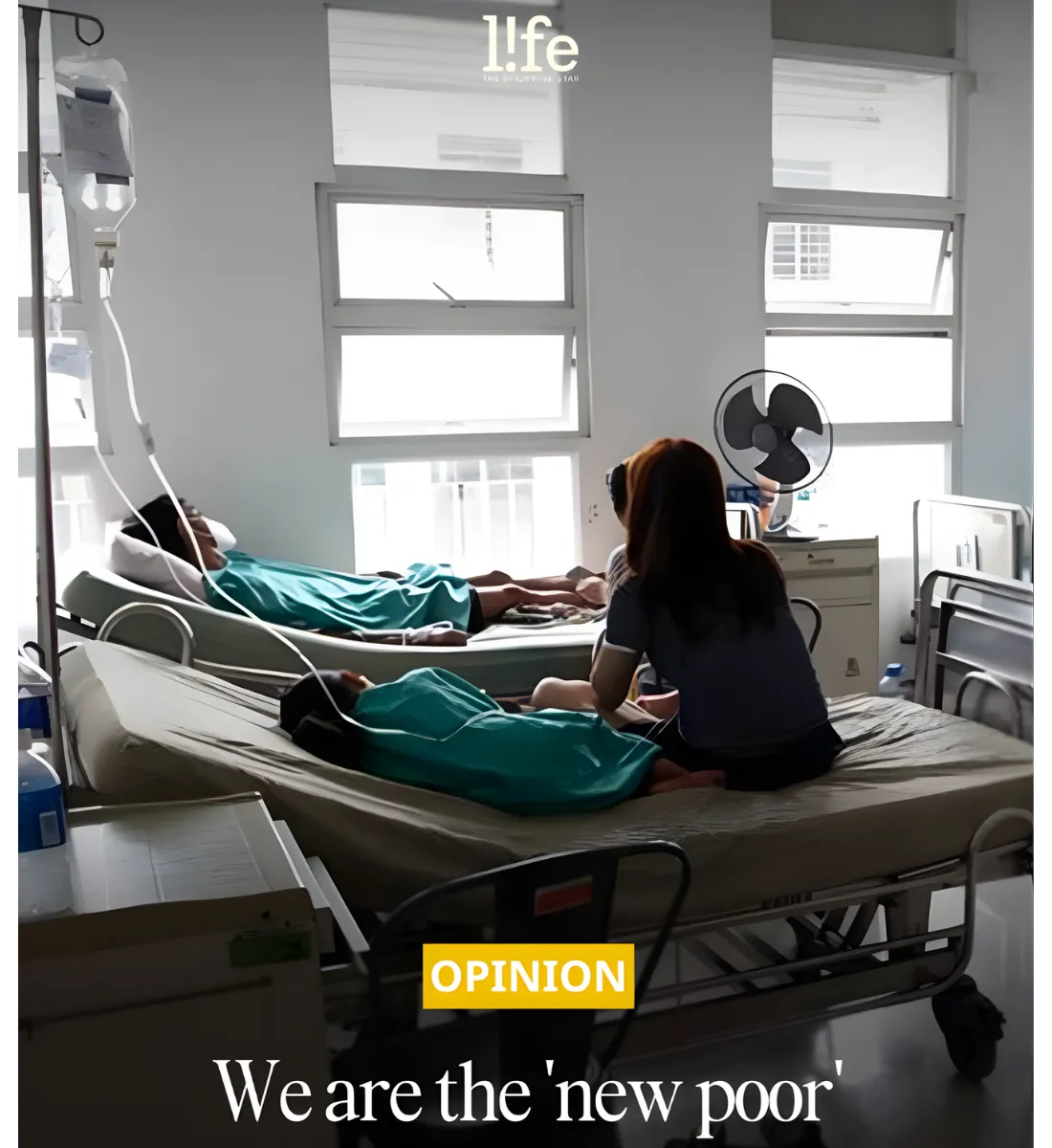

A reminder to prepare—not just react—when health emergencies strike.

A few days ago, veteran columnist Cito Beltran shared a heartbreaking story:

A father—an ordinary, hardworking Filipino with a stable job—was forced to beg for help because his son needed urgent surgery. Even with an HMO, PhilHealth, and personal savings, the costs were still overwhelming. Their last resort? Swipe their credit cards, skip Christmas, and hope they can survive the debt later.

Sadly, this is no longer unusual.

This is now the Filipino reality.

The Harsh Truth: Middle-Class Families Are Now “The New Poor”

Many of us think that because we’re employed, have PhilHealth, and maybe even an HMO, we are safe.

But the truth?

👉 Minor to medium surgeries can easily cost ₱200,000 to ₱600,000 today.

👉 Doctor’s professional fees alone can reach six figures.

👉 Private hospital charges feel like daily ATM withdrawals.

Before we know it, the savings we worked so hard for disappear overnight.

We’re lining up at LGUs, asking PCSO for help, and swiping credit cards out of desperation.

And while government hospitals like Rizal Medical Center are improving (as Cito himself experienced), the system is still stretched thin. We can’t rely solely on it—not when corruption, underfunding, poor planning, and outdated facilities continue to slow things down.

So What Can We Do?

We prepare.

We stop depending solely on PhilHealth or HMOs that were never designed to cover everything.

And we stop assuming that emergencies won’t happen to us.

If you’re employed, self-employed, or earning steadily, this is the best time to ask yourself:

“If someone in my family needed surgery tomorrow, can I really afford it?”

If your answer makes you uncomfortable, then you're already getting the message.

Health Emergencies Should Not Push Families Into Poverty

We shouldn’t have to:

❌ Beg for help

❌ Skip Christmas

❌ Sell cars

❌ Pawn land titles

❌ Stack credit card debt

Just to save the people we love.

But this is what happens when we prepare late.

And this is exactly why products like FWD Set for Health and FWD Vibrant exist—not to take advantage of weakness, but to give Filipinos a fighting chance.

Why Consider FWD Set for Health and Vibrant?

Because these plans give you:

✔ Lump-sum cash for diagnosis of critical illness

✔ No need to show hospital receipts

✔ Freedom to choose where you want to be treated—private or public

✔ Protection from future medical inflation

✔ Coverage that HMOs and PhilHealth simply cannot match

In short:

They protect your savings, your dignity, and your family from becoming the “new poor.”

and a Health Supplement Benefit that provides 2% of the benefit amount monthly for six months upon the first major critical illness claim.")

We Can’t Control the System, But We Can Control Our Preparation

The government still has a long journey in fixing public healthcare.

Corruption, lack of funding, and slow project completion will not disappear soon.

Even with improvement, public hospitals are overcrowded because so many Filipinos now can’t afford private care.

So instead of waiting for the system to save us,

we save ourselves first.

Final Thoughts

Cito Beltran was right:

Many working Filipinos are unknowingly just one health emergency away from poverty.

But we don’t need to stay vulnerable.

If you're earning today, make this the year you set aside a portion of your income to protect your own future. Because no matter how strong or responsible we are, medical emergencies don’t wait for perfect timing.

And when that day comes, you will thank yourself for preparing early.

Are you Ready to secure your health protection for 2026?

Book a Private Financial Strategy Session with me — a 20-minute guided call to:

✔ Check if your current HMO + PhilHealth coverage is enough

✔ Identify gaps sa medical protection mo

✔ Create a health security plan that fits your budget

✔ Explore FWD Set for Health & Vibrant options

Limited slots only.

Book your schedule here: Quick Coverage Check